What to Expect with Your UMortgage Loan Process

April 18, 2024

What to Expect with Your UMortgage Loan Process

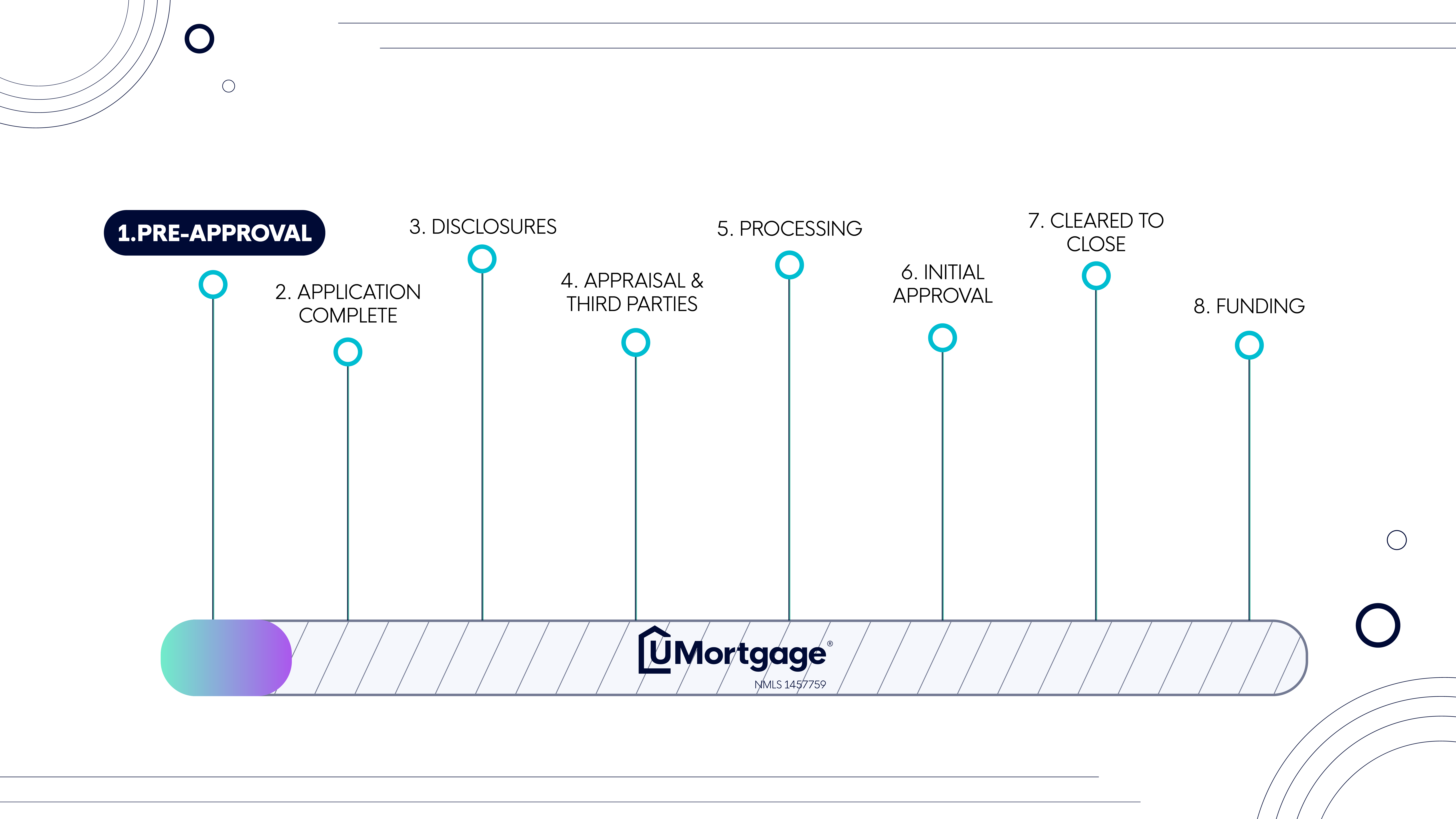

Mortgages can be complicated. That’s why, at UMortgage, we’ve broken down the loan process into 8 easy digestible steps. A strong buyer is a well-informed buyer, so to help you know what to expect every step of the way, let's walk you through the 8-step mortgage process from pre-approval to your first mortgage payment.

Step 1: Pre-Approval

To set yourself up for a successful homebuying experience, you must first work with your UMortgage Loan Originator to get pre-approved for your future home loan. Not only will your pre-approval give you an accurate budget to help you shop for homes, but it will also expedite your approval process once you’ve had an offer accepted on your home-to-be.

Your pre-approval is a document from your lender stating that they are willing to let you borrow a certain loan amount based on your creditworthiness, income, and other financial considerations. In a competitive housing market, a strong pre-approval can go a long way to help you stand out among the sea of competing offers. This first step demonstrates that you are a serious buyer by proving that a lender is willing to provide the loan necessary to purchase the property on your shopping list.

Once you’re pre-approved, you will have a quoted figure that you can use to help yourself narrow down your home search to those that are in your budget. Pre-approvals typically last up to 90 days, so be in contact with your UMortgage LO as you shop to make sure your pre-approval is up to date for a smooth homebuying process!

Step 2: Application Submitted

Once you’ve worked with a real estate agent to shop for homes and have had your offer accepted, it’s time to apply for a mortgage! This is where your pre-approval will come in handy because the financial documents that are used for your pre-approval are the same documents needed to apply for your mortgage.

When you’re filling out your mortgage application, you can talk with your UMortgage LO to figure out the loan product that will work best for your financial situation. Once your application is complete and submitted, our Operations team will verify your credit, income, and other supporting documentation submitted with your application.

Step 3: Disclosures

The next step for your loan is disclosures. This step provides you with an overview of the specificities regarding your loan, including your loan terms, mortgage rate, rights, and a full breakdown of all fees associated with your mortgage.

After your application and documentation have been verified, it moves to disclosures. During disclosures, our Operations team compiles estimates for all fees associated with your mortgage, including title fees, closing costs, and other third-party fees.

Once all necessary fees have been confirmed, your loan disclosure will be sent. This document outlines your loan amount, mortgage rate, required down payment, closing costs, and estimates of third-party fees. When you receive this document, it’s crucial that you sign these documents as quickly as possible to avoid any delays and get you into your home faster. After signing your closing disclosure, your loan team will order an appraisal and all third-party services.

Step 4: Appraisal & Third Parties

As your loan awaits processing, UMortgage orders an appraisal on the home and any other requested third-party services such as an inspection, title services, and more.

Appraisals assess the fair market value of the property being purchased. Lenders require an appraisal to be conducted on every property they’re helping finance to ensure that the property is worth the amount of money being loaned to the borrower. This step protects you and the lender from overpaying or lending more than the property's actual value.

Appraisals are conducted by certified and impartial third-party professionals who have no vested interest in the outcome of the transaction. These third-party appraisers thoroughly evaluate various aspects of the property, including its size, condition, location, and comparable sales in the area.

Step 5: Processing

When your loan is in processing, it’s being assessed by a Processor on our Operations team. The Processor’s job is to ensure all financial documents associated with your loans are accurate and verified. Throughout the processing phase, you may be contacted by your loan’s Processor with any updates and requests for other supplementing documents to ensure your loan passes underwriting and is approved.

Once they receive your loan, your Processor will be your main point of contact. You can expect them to reach out for a formal introduction when your loan enters Processing.

As soon as all the necessary information has been collected and approved by the processor, they will submit your loan to the lender’s underwriters who do one final review of all the documentation before deciding to approve or deny the mortgage.

Step 6: Initial Approval

After your loan is approved by underwriting, your next step in the loan process is initial approval. During this stage, your UMortgage team might reach out for a few more pieces of documentation to get your loan across the finish line. These requests are a completely normal part of this step in the mortgage process, so don’t panic if you’re asked to send new or updated documents!

After all conditions have been met, you’ll get your final closing disclosure which, like your initial closing disclosure, outlines your loan amount, mortgage rate, closing costs, and all other fees that you’re required to pay to close your loan. Unlike your initial closing disclosure, the figures on your final closing disclosure are the exact fees and terms associated with your mortgage. When you sign your closing disclosure, you’ll close three days later.

Step 7: Cleared to Close

When you’ve reached step #7, your loan is cleared to close! This means that you’re one final step away from homeownership! When a loan is cleared to close, that means it has passed underwriting and been fully approved by your lender.

Before you head to your appointment to sign the final paperwork and close on your home, you’ll need to secure the required funds that have been outlined in your final signed closing disclosure. You’ll pay these funds with either a cashier’s check or a wire transfer.

Please note that you will NEVER receive wire instructions from a UMortgage team member. If you do, please report it immediately. Only your Title company will reach out with wiring instructions once your loan is cleared to close.

Closings most commonly take place at a title company or real estate office with your real estate agent, title agent, the seller’s agent, and any co-borrowers purchasing the home with you.You’ll need to bring a state-issued photo ID and all documentation related to your purchase, including proof of homeowner’s insurance and a copy of your purchase contract.

Expect to spend up to an hour at the closing table, carefully reviewing and signing a multitude of documents, including the mortgage agreement, title deed, and various disclosures. Once this paperwork has been signed, the keys are handed over and you’re officially the owner of your new home!

Step 8: Funding

The final step of your mortgage process is the funding of your loan. Here, your lender contacts the seller’s agent to distribute the funds needed to complete the purchase of your home. After funding, you’ll hear from your UMortgage LO with more information on paying your first mortgage payment and a request for feedback on your mortgage experience.

Your first mortgage payment will likely be due the first of the month 30 days after your closing date. So, if you closed on April 10th, your first mortgage payment would be due on June 1st.

When it comes time to make your first mortgage payment, please take a look at the final documents signed at closing for all the details including your exact payment and due date. You also may receive correspondence from the new servicer via email or postal mail about where and how to make future mortgage payments. If you have any questions about your mortgage payment, feel free to contact your UMortgage Loan Originator.

Finally, purchasing a home is part of the public record. After you close, you will most likely receive various forms of spam. Wire fraud is on the rise in the mortgage industry and the last thing we want is for you to become a victim.